Fintech startups across the world began life by unbundling banking services, with startups specialising in single segments. As the space develops and matures, however, this is changing.

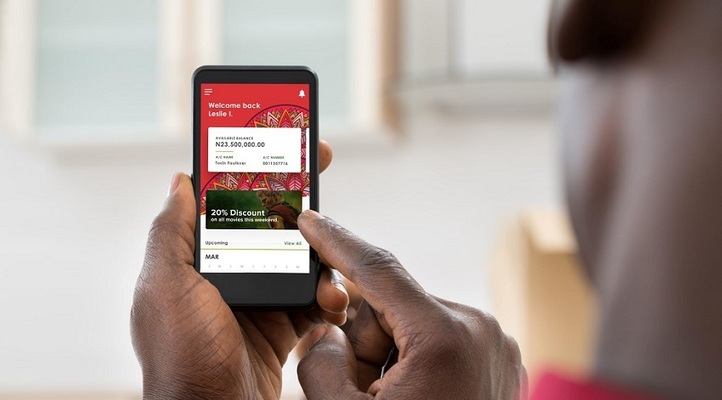

Now, we have entered the era of rebundling. Whereas fintechs made waves by deconstructing the bank, going niche rather than adopting a supermarket, one-stop-shop approach, increasingly they are changing tack. In Africa, where traditional banks have failed to bring about financial inclusion, digital banks may yet.

This is confirmed by the findings of Disrupt Africa’s recently-released Finnovating for Africa 2019 report, which finds that an increasing number of African fintech startups are operating across multiple verticals.

The trend towards rebundling the bank is most evident in Nigeria. TeamApt secured a switching license from the Central Bank of Nigeria off the back of raising a US$5.5 million Series A round, OneFi, which itself raised US$5 million in funding, acquired payments solution Amplify as it continues its progress towards becoming a full service digital bank, which also involved rebranding its Paylater product as Carbon. Kudi, meanwhile, is also expanding its offering after securing investment.

As more fintech startups raise funding, and therefore increase their capacity, we can expect to see more of this. According to the African Tech Startups Funding Report 2018 released by Disrupt Africa, a total of 58 fintech startups raised funding over the course of last year, more than any other sector, while the US$132.8 million raised by African fintech startups was almost 40 per cent of the overall total. With funding increasing exponentially, so to will the number of fintechs adding to their offerings and aspiring to be full digital banks.

Sourced through Scoop.it from: disrupt-africa.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment